POLICY AND PROCEDURES FOR REPORTING POSSIABLE IMPROPRIETIES IN MATTERS OF FINANCIAL REPORTING OR OTHER MATTERS

WHISTLE BLOWER POLICY

The Audit Committee of the Board of Directors of GDS Holdings Limited (the “Company”) has established the following procedures for the receipt, retention, investigation and treatment of complaints and concerns regarding accounting, internal accounting controls, auditing and other legal matters.

I. Scope

A. The procedures set forth in this Policy relate to complaints and concerns of employees and other interested parties, including shareholders, (each referred to in this Policy as a “Complainant”) of the Company, its subsidiaries and consolidated entities (“Reports”) regarding:

1. questionable accounting, internal accounting controls or auditing matters (an “Accounting Allegation”), including, without limitation:

(a) fraud or deliberate error in the preparation, evaluation, review or audit of financial statements of the Company;

(b) fraud or deliberate error in the recording and maintaining of the Company’s financial records;

(c) the circumvention or attempted circumvention of internal accounting controls;

(d) deficiencies in, or non-compliance with, the Company’s internal control over financial reporting or accounting policies;

(e) any misrepresentation or false statement regarding a matter contained in the Company’s financial records, financial statements, financial reports (including discussions in an annual reports filed with the Securities and Exchange Commission (the “SEC”)), or audit reports, or any other failure to provide a full or fair reporting of the Company’s financial condition;

(f) deviation from full and fair reporting of the Company’s financial condition and results;

(g) substantial variation in the Company’s financial reporting methodology from prior practice or from generally accepted accounting principles;

(h) issues affecting the independence of the Company’s independent registered public accounting firm;

(i) falsification, concealment or inappropriate destruction of corporate or financial records;

2. non-compliance with applicable legal and regulatory requirements, including without limitation, the rules and regulations promulgated by the SEC and the Listed Company Manual of the New York Stock Exchange (to the extent applicable), or the Company’s Code of Business Conduct and Ethics (a “Legal Allegation”) which is posted and accessible by all employees via internal Office Automation system; and

3. retaliation against employees and other persons who make, in good faith, Accounting Allegations or Legal Allegations (a “Retaliatory Act”).

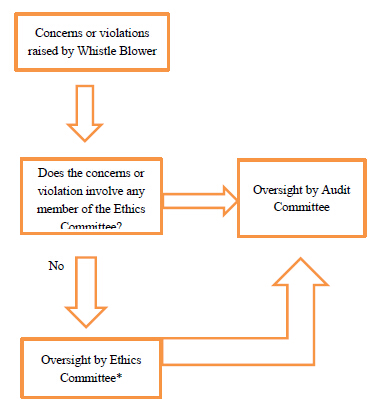

B. In the discretion of the Audit Committee, responsibilities of the Audit Committee created by these procedures may be delegated to Ethics Committee, a subcommittee of the Audit Committee.

Ethics Committee, shall mean a committee comprising of the Chief Executive Officer (CEO), Chief Finance Officer (CFO), Head of Human Resource and General Counsel (or their respective equivalents). The CEO (or his equivalent) will be appointed as the chairman of the Ethics Committee.

The Ethics Committee shall address questions and concerns raised and provide oversight to investigation of concerns or violations of matters not involving any members of the Ethics Committee as well as implement measures of rectification and prevention. If the concern or violation involves the department of any Ethics Committee member, he or she shall recuse himself or herself from overseeing the investigation of such concerns or violations and the remaining members of the Ethics Committee shall have oversight over such investigations.

In line with good corporate governance practices, all concerns or violations raised and cases of "whistle blowing" will be reported to and reviewed by the Company’s Audit Committee. For matters involving any members of the Ethics Committee, the investigation will be directly supervised by the Audit Committee. Please refer to Appendix.

II. Procedures for Making Complaints

A. In addition to any other avenue available, any employee may, in his or her sole discretion, report to the Audit Committee or the compliance officer appointed by the Board (the “Compliance Officer”) openly, confidentially or anonymously, any Accounting Allegation, Legal Allegation or Retaliatory Act:

1. In writing to the Company, Attn: 5F Tower C, Sunland International, 999 Zhouhai Rd, Pudong New District, Shanghai 200137, P.R.C.;

2. by sending an e-mail to Ethics@gds-services.com;

3. by calling the hotline or leave a voice mail at +86-021-5831 5858.

B. Any other interested party may report to the Audit Committee or the Compliance Officer any Accounting Allegation, Legal Allegation or Retaliatory Act, as set forth in Section II.A. above. Any such Report must be accompanied by the name of the person submitting the Report. Where permitted by law, your phone calls and reports may be made anonymously. However, anonymous feedback will not be accorded the same level of attention by the Audit Committee of the Company.

C. The Reports should be factual rather than speculative or conclusory, and should contain as much specific information as possible to allow for proper assessment. In addition, all Reports should contain sufficient corroborating information to support the commencement of an investigation, including, for example, the names of individuals suspected of violations, the relevant facts of the violations, how the Complainant became aware of the violations, any steps previously taken by the Complainant, who may be harmed or affected by the violations, and, to the extent possible, an estimate of the misreporting or losses to the Company as a result of the violations.

III. Procedures upon Receipt of a Report

A. The Compliance Officer should, upon receipt of a Report and when possible and appropriate, acknowledge receipt to the Complainant who submitted it.

B. All Reports sent to the Compliance Officer must promptly undergo an initial review by Audit Committee and the Compliance Officer, who must:

1. promptly forward to the Audit Committee any report involving the Company’s senior officials or having an actual or potential misreporting or loss to the Company that could have a material adverse effect on the Company’s reputation or financial statements; and

2. promptly determine whether to commence an investigation of all other Reports:

(a) the Compliance Officer may, in his/her reasonable discretion, determine not to commence an investigation if the Report contains only unspecified or broad allegations of wrongdoing without appropriate informational support or if the Report is not credible. This decision shall be reported to the Audit Committee at its next ordinary meeting and shall, to the extent appropriate, be made known to the Complainant who submitted the Report. The Audit Committee may, however, not accept this decision, in which case it will determine whether the Audit Committee or the Compliance Officer will investigate the Report, taking into account the factors described in Section IV.B.2. below; and

(b) If the Compliance Officer determines that an investigation must be conducted, he/she will promptly commence the investigation. The Compliance Officer shall also promptly investigate other Reports as requested in writing by the Audit Committee. The Compliance Officer shall report the findings of the investigations conducted pursuant to this section to the Audit Committee in accordance with Section III.D.

C. the Compliance Officer may consult with any other member of management who is not the subject of the Accounting Allegation, Legal Allegation or Retaliatory Act included in the Report and who may have appropriate expertise to provide assistance in connection with the investigation of the Report. The Compliance Officer may also engage independent accountants, counsel or other experts to assist in the investigation of Reports and analysis of results, if necessary or appropriate.

D. the Compliance Officer shall, provide a monthly report to Audit Committee following by a conference call. Additionally, at every Audit Committee’s ordinary meeting, present a summary of all the Reports received by, or forwarded to, her/him (including those Reports that she/he decided not to investigate) and all the material developments, findings and conclusions of investigations since the previous meeting. The Audit Committee may or may not accept such findings and conclusions. The Compliance Officer shall provide such additional information regarding any Report or investigation as may be requested by the Audit Committee.

IV. Procedures upon Complaint Report received, or Forwarded to, the Audit Committee

A. The Audit Committee should, upon receipt of a report directly from a Complaint and when possible and appropriate, acknowledge, or direct the Compliance Officer to acknowledge, receipt of the Report to the Complainant who submitted it.

B. All Reports received directly by the Audit Committee or pursuant to Section III.B.1. above must promptly undergo a review by the Audit Committee:

1. The Audit Committee may, in its reasonable discretion, determine not to commence an investigation if a Report contains only unspecified or broad allegations of wrongdoing without appropriate informational support or the Report is not credible. This decision shall, to the extent appropriate, be made known to the Complainant who submitted the Report.

2. If the Audit Committee determines that an investigation should be conducted, the Audit Committee shall determine whether the Audit Committee or the Compliance Officer should investigate the Report, taking into account, among other factors that are appropriate under the circumstances, the following:

(a) Who is the alleged wrongdoer? If an executive officer, senior financial officer or other high management official is alleged to have engaged in wrongdoing, that factor alone may militate in favor of the Audit Committee conducting the investigation.

(b) How material is the misreporting or loss? The more material the misreporting or loss to the Company, the more appropriate it may be that the Audit Committee should conduct the investigation.

(c) How serious is the alleged wrongdoing? The more serious the alleged wrongdoing, the more appropriate that the Audit Committee should undertake the investigation. If the alleged wrongdoing would constitute a crime involving the integrity of the financial statements of the Company or would have a material adverse effect on the Company’s reputation or financial statements, that factor alone may militate in favor of the Audit Committee conducting the investigation.

(d) How credible is the allegation of wrongdoing? The more credible the allegation, the more appropriate that the Audit Committee should undertake the investigation. In assessing credibility, the Audit Committee should consider all facts surrounding the allegation, including, but not limited to, whether similar allegations have been made in the press or by analysts.

C. If the Audit Committee determines that the Compliance Officer should investigate the Report, the Audit Committee will notify the Compliance Officer in writing of that conclusion. The Compliance Officer shall thereafter promptly investigate the Report and shall report the results of the investigation to the Audit Committee in accordance with Section III.D. In the other cases, the Audit Committee shall promptly investigate the Report.

D. The Audit Committee may consult with any member of management who is not the subject of the Accounting Allegation, Legal Allegation or Retaliatory Act included in the Report and who may have appropriate expertise to provide assistance. The Audit Committee may also engage independent accountants, counsel or other experts to assist in the investigation of Reports and analysis of results.

V. Results of Investigation

A. Upon completion of the investigation of a Report:

1. the Audit Committee or the Compliance Officer, as the case may be, will take such prompt and appropriate corrective action, if any, as in its/his/her judgment is deemed warranted; and

2. the Audit Committee or the member of management, as the case may be, will contact, to the extent appropriate, each Complainant who files a Report to inform him/her of the results of the investigation and what, if any, corrective action was taken.

B. Where alleged facts disclosed pursuant to this Policy are not substantiated, the conclusions of the investigation shall, to the extent appropriate, be made known to the Complainant who made the Report.

C. No action will be taken against any Complainant who makes a Report in good faith, even if the facts alleged are not confirmed by subsequent investigation. However, if, after investigation, a Report is found to be without substance and to have been made for malicious or frivolous reasons, the employees who made the Report could be subject to disciplinary action, up to, and including, termination of employment.

VI. Protection of Whistleblowers

A. Neither the Company, the Audit Committee nor any director, officer or employee of the Company will discharge, demote, suspend, threaten, harass, directly or indirectly, or in any other manner discriminate or retaliate, directly or indirectly, against any person who, in good faith, makes a Report or otherwise assists the Audit Committee, management or any other person or group, including any governmental, regulatory or law enforcement body, in investigating a Report.

B. Unless necessary to conduct an adequate investigation or compelled by judicial or other legal process, neither the Company, the Audit Committee nor any director, officer or employee of the Company shall (i) reveal the identity of any person who makes a Report and asks that his or her identity remain confidential, or (ii) make any effort, or tolerate any effort made by any other person or group, to ascertain the identity of any person who makes a Report anonymously.

VII. Records

The Audit Committee and the Compliance Officer shall maintain a log of all records relating to any Reports of Accounting Allegation, Legal Allegation or Retaliatory Act, tracking their receipt, investigation and resolution and the response to the person making the Report. The Company shall retain copies of the reports and records for a period of seven years.

Endorsed by Audit Committee and Board of Directors, approved in September 2015.

This policy is promulgated in November 2015.

APPENDIX

* If the concern or violation involves the department of any Ethics Committee member, he or she shall recuse from overseeing the investigation of such concerns or violations and the remaining of the Ethics Committee shall have oversight over such investigations.

京公网安备 11010502051891号

京公网安备 11010502051891号